Global Turmeric Milk Mix Market Growth Driven by Growing Consumer Preference for Herbal Functional Beverages and Premium Wellness Nutrition

Market Overview

The Global Turmeric Milk Mix Market is experiencing significant growth driven by increasing consumer awareness of holistic health, rising demand for immunity-supporting beverages, expanding interest in Ayurvedic nutrition, and growing consumption of clean-label functional food products. Turmeric milk mix products are gaining popularity among consumers seeking convenient, nutritious beverages that combine traditional wellness ingredients with modern lifestyles. Product innovation across organic, dairy-free, fortified, low-sugar, and flavored variants is expected to accelerate market growth throughout the forecast period.

Get Full PDF Sample Copy of Report:

https://www.maximizemarketresearch.com/request-sample/280507/

Technology and Innovation Landscape

Technological advancements are enhancing the turmeric milk mix market through improved ingredient processing, functional fortification, and sustainable manufacturing practices.

Innovations such as bioavailability-enhanced curcumin formulations, instant dissolving turmeric blends, organic ingredient sourcing, plant-based milk alternatives, probiotic- and adaptogen-infused formulations, vitamin- and mineral-fortified products, low-sugar recipes, spray-drying and freeze-drying technologies, recyclable and biodegradable packaging, AI-powered quality assurance systems, and personalized nutrition solutions are increasingly being adopted. These innovations improve nutritional performance, convenience, shelf life, product consistency, and consumer satisfaction.

Largest Market Segment Analysis

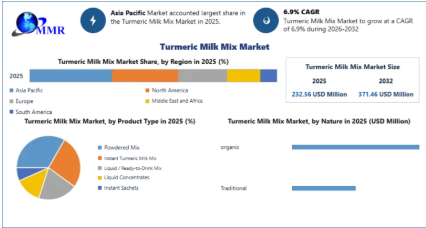

The Powdered Turmeric Milk Mix Segment continues to dominate the market owing to its long shelf life, affordability, ease of storage, convenient preparation, and broad distribution through supermarkets, pharmacies, specialty stores, and online retail platforms.

Its practicality and widespread consumer acceptance continue to reinforce its market leadership.

Fastest-Growing Segment Analysis

The Fortified Turmeric Milk Mix Segment is expected to witness the fastest growth due to increasing demand for products enriched with vitamins, minerals, probiotics, and botanical ingredients that provide additional health benefits.

Growing consumer interest in preventive nutrition and daily wellness is accelerating segment growth.

Regional Insights

Asia Pacific remains the dominant regional market owing to deep-rooted consumption of turmeric beverages, rising disposable incomes, increasing awareness of Ayurvedic wellness, and expanding retail availability across India, China, Japan, and Southeast Asia.

North America maintains a substantial market share supported by growing consumer demand for functional beverages, herbal nutrition products, and clean-label dietary solutions.

Europe is expected to witness the fastest growth due to increasing preference for organic beverages, plant-based nutrition, sustainable food products, and natural wellness ingredients.

Competitive Landscape

Key players

Global:

Nestlé S.A.

Organic India Pvt. Ltd.

Gaia Herbs

Four Sigmatic

Nature's Way Products LLC

Get Full PDF Sample Copy of Report:

https://www.maximizemarketresearch.com/request-sample/280507/

Market Dynamics

The market is driven by increasing health consciousness, rising demand for immunity-supporting beverages, growing popularity of Ayurvedic nutrition, and continuous innovation in functional food and beverage products.

However, challenges such as fluctuating turmeric prices, strict food safety regulations, competition from alternative wellness beverages, and raw material supply fluctuations may restrain market growth.

Despite these challenges, increasing investments in premium organic product development, expansion of digital retail channels, growing demand for personalized nutrition, and continuous innovation in fortified wellness beverages are expected to create significant growth opportunities.

Get access to the full description of the report:

https://www.maximizemarketresearch.com/market-report/turmeric-milk-mix-market/280507/

About Maximize Market Research

Maximize Market Research Pvt. Ltd. is a global market intelligence and consulting firm delivering data-driven insights and comprehensive industry analysis across food & beverages, nutrition, consumer goods, healthcare, wellness, and functional food markets.

Global Turmeric Milk Mix Market Growth Driven by Growing Consumer Preference for Herbal Functional Beverages and Premium Wellness Nutrition

Market Overview

The Global Turmeric Milk Mix Market is experiencing significant growth driven by increasing consumer awareness of holistic health, rising demand for immunity-supporting beverages, expanding interest in Ayurvedic nutrition, and growing consumption of clean-label functional food products. Turmeric milk mix products are gaining popularity among consumers seeking convenient, nutritious beverages that combine traditional wellness ingredients with modern lifestyles. Product innovation across organic, dairy-free, fortified, low-sugar, and flavored variants is expected to accelerate market growth throughout the forecast period.

Get Full PDF Sample Copy of Report:

https://www.maximizemarketresearch.com/request-sample/280507/

Technology and Innovation Landscape

Technological advancements are enhancing the turmeric milk mix market through improved ingredient processing, functional fortification, and sustainable manufacturing practices.

Innovations such as bioavailability-enhanced curcumin formulations, instant dissolving turmeric blends, organic ingredient sourcing, plant-based milk alternatives, probiotic- and adaptogen-infused formulations, vitamin- and mineral-fortified products, low-sugar recipes, spray-drying and freeze-drying technologies, recyclable and biodegradable packaging, AI-powered quality assurance systems, and personalized nutrition solutions are increasingly being adopted. These innovations improve nutritional performance, convenience, shelf life, product consistency, and consumer satisfaction.

Largest Market Segment Analysis

The Powdered Turmeric Milk Mix Segment continues to dominate the market owing to its long shelf life, affordability, ease of storage, convenient preparation, and broad distribution through supermarkets, pharmacies, specialty stores, and online retail platforms.

Its practicality and widespread consumer acceptance continue to reinforce its market leadership.

Fastest-Growing Segment Analysis

The Fortified Turmeric Milk Mix Segment is expected to witness the fastest growth due to increasing demand for products enriched with vitamins, minerals, probiotics, and botanical ingredients that provide additional health benefits.

Growing consumer interest in preventive nutrition and daily wellness is accelerating segment growth.

Regional Insights

Asia Pacific remains the dominant regional market owing to deep-rooted consumption of turmeric beverages, rising disposable incomes, increasing awareness of Ayurvedic wellness, and expanding retail availability across India, China, Japan, and Southeast Asia.

North America maintains a substantial market share supported by growing consumer demand for functional beverages, herbal nutrition products, and clean-label dietary solutions.

Europe is expected to witness the fastest growth due to increasing preference for organic beverages, plant-based nutrition, sustainable food products, and natural wellness ingredients.

Competitive Landscape

Key players

Global:

Nestlé S.A.

Organic India Pvt. Ltd.

Gaia Herbs

Four Sigmatic

Nature's Way Products LLC

Get Full PDF Sample Copy of Report:

https://www.maximizemarketresearch.com/request-sample/280507/

Market Dynamics

The market is driven by increasing health consciousness, rising demand for immunity-supporting beverages, growing popularity of Ayurvedic nutrition, and continuous innovation in functional food and beverage products.

However, challenges such as fluctuating turmeric prices, strict food safety regulations, competition from alternative wellness beverages, and raw material supply fluctuations may restrain market growth.

Despite these challenges, increasing investments in premium organic product development, expansion of digital retail channels, growing demand for personalized nutrition, and continuous innovation in fortified wellness beverages are expected to create significant growth opportunities.

Get access to the full description of the report:

https://www.maximizemarketresearch.com/market-report/turmeric-milk-mix-market/280507/

About Maximize Market Research

Maximize Market Research Pvt. Ltd. is a global market intelligence and consulting firm delivering data-driven insights and comprehensive industry analysis across food & beverages, nutrition, consumer goods, healthcare, wellness, and functional food markets.